RealtyShares recently announced that it had closed a $28M Series C that the company plans to use to expand its crowdfunding platform to better cater to high net worth individuals and institutions looking to access new tiers of the real estate investment market.

Founded in 2013, RealtyShares connects accredited investors looking to put money into commercial or residential real estate, with real estate developers looking to raise capital. The company says it has 120,000 users on its platform, who have invested $500 million since the company's inception.

RealtyShares recently announced that it had closed a $28M Series C that the company plans to use to expand its crowdfunding platform to better cater to high-net-worth individuals and institutions looking to access new tiers of the real estate investment market.

Founded in 2013, RealtyShares connects accredited investors looking to put money into commercial or residential real estate, with real estate developers looking to raise capital. The company says it has 120,000 users on its platform, who have invested $500 million since the company's inception.

Key Growth Lessons

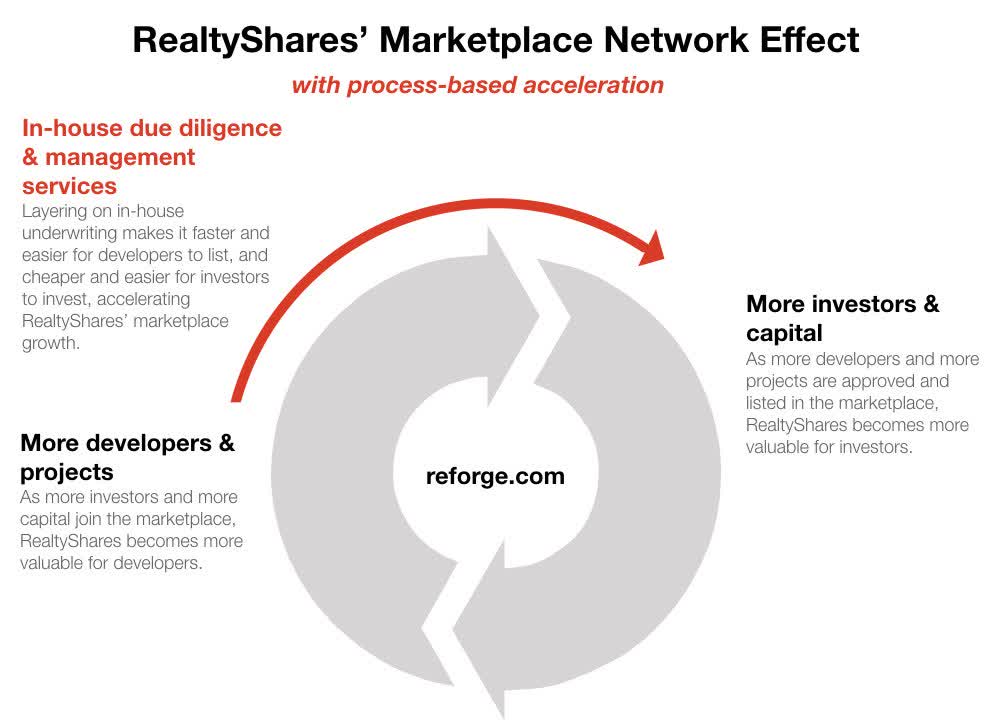

1. RealtyShares built supply-side density through process-based innovations, which enabled growth and network effects within the marketplace as a whole.

RealtyShares' process innovations — most notably, vertical ownership of the tedious underwriting process for real estate investment projects — makes it faster and easier to list projects on the platform, enabling the company to build up rapid supply side density, which triggers growth on the demand side.

2. By aggregating smaller investments in “18-hour cities,” the company is able to open up new supply that wouldn't otherwise have been profitable or efficient for investors.

RealtyShares is increasingly going after smaller commercial deals in growth markets that would have been too small for major investors to consider. As it aggregates these deals, and adds a layer of support services (including but not limited to due diligence), it makes it more efficient for big investors to get involved.

3. Moving upmarket to monetize

The investment/funding platform's monetization model is based on transaction size, but legal constraints reign in the number of investors a given project can take in. To grow monetization under their current model, RealtyShares has just one route — to go after better-capitalized investors while offering them bigger investment projects made efficient through aggregation.

The details behind these takeaways are outlined in the rest of this piece.

Faster supply-side acquisition leads to faster growth

RealtyShares aggregates smaller real estate opportunities that normally wouldn't be cost efficient for big investors to get into. The company then underwrites the deals themselves, and by handling a lot of the red tape admin in house (that's what all that VC money is for), they're able to accelerate the speed at which deals get done. It takes on average just 4 days for real estate developers who list opportunities on the platform to see their projects get fully funded.

This funding flow makes it profitable for investors to put in as little as $5K into projects that might otherwise have been too time- and resource-intensive for investors to run their own due diligence process.

Additionally, RealtyShares is increasingly going after smaller commercial deals in “18 Hour Cities” — growth markets that are one tier below big, expensive cities like New York and San Francisco — that have historically been outside the scope of the largest institutional investors.

As the company aggregates these deals, and adds on its own layer of support services (including but not limited to due diligence), it makes it more efficient for big investors to get involved.

Meanwhile, by opening up — and speeding up — access to new, alternative capital, the company presents an appealing alternative, or supplement, to traditional lenders for developers looking to raise debt or equity for a project. A developer may have a loan from the bank, but loan terms may require that the developer put up a substantial chunk of their own funds. That's where crowdfunding platforms come in.

All of this leads to faster transaction cycles and positively impacts liquidity in their marketplace:

More importantly for investors, RealtyShares has already returned some of their capital, enabling them to re-invest in new projects on its platform.

As more investor money flows in to the network, more developers jump in to RealtyShares' (relatively speedy) supply side onboarding.

As the more qualified developers join and bring in more vetted projects, RealtyShares is able to offer more options for investors' money, and the platform's match rate gets better and better.

Moving upmarket to monetize

Although the company started out as a “crowdfunding” platform aimed to lower the barrier to entry for real estate investing (and borrowing), its CEO Nav Athwal now emphasizes that RealtyShares is refocusing its gaze to target more upmarket investors — including institutions.

This makes sense given the company's monetization model, and its competitive landscape.

RealtyShares makes money from both sides of its marketplace. On the investor side, it charges a management fee on assets. On the developer side, it charges a one-time placement fee (calculated as a percentage based on deal size).

Because the same costly underwriting process applies to a $5M project as to a $50M project, it's to the company's benefit to go after bigger deals that net them greater fees on both sides.

But, Section 3(c)(1) of the Investment Company Act constrains the total number of participants in any given project to 100 investors or fewer. That means, in order for companies like RealtyShares to take on a $100M commercial real estate project, they would need 100 investors willing to put in $1M each. This is not only well beyond their $5K qualifying minimum, but also a much larger sum than most individual (non-HNWI) investors are able or willing to risk.

So, in order for RealtyShares to go after the highest-ROI deals for the company, it needs to shift upmarket in order to bring in those investors who can allocate significant capital — and who are unlikely to want to take it out of circulation on the platform anytime soon.

As the company onboards more well-capitalized investors, it also attracts more and higher quality development projects. Because RealtyShares has been busy gobbling up variety on its supply side, it now offers the most diverse array of options across key categories (debt vs. equity, geography, and property types) versus its competition. More inventory on its “shelves” not only paves its monetization path, but also contributes to its growing marketplace network effect.