Chinese restaurant-ordering giant Meituan-Dianping recently raised $4B at a $30B valuation, making it the 5th most valuable unicorn in the world (and the 3rd most valuable in China).

In this 5-min read, we’ll look at the techniques that Meituan-Dianping used to overcome growth and monetization challenges faced by peers in the US, including Yelp, Groupon, and others.

Chinese restaurant-ordering giant Meituan-Dianping recently raised $4B at a $30B valuation, making it the 5th most valuable unicorn in the world (and the 3rd most valuable in China).

In this 5-min read, we’ll look at the techniques that Meituan-Dianping used to overcome growth and monetization challenges faced by peers in the US, including Yelp, Groupon, and others.

Key Growth Lessons

1. Reviews are a traffic acquisition engine, while deals monetize.

Meituan's 2015 merger with Dianping enabled the company to leverage each vertical's strengths to make up for another vertical's weaknesses.

For example, while restaurant reviews are notoriously tough to monetize on an impression basis, they do bring enormous amounts of cheap traffic. That traffic can be better monetized by Groupon-style deals, which sell something relevant directly to the consumer.

At the same time, its reservation system creates a defensive moat that keeps restaurants on board, while food delivery leverages those restaurant relationships into an additional high-growth line of business.

2. Dominate neighboring verticals, then use that distribution and infrastructure firepower to expand into more distant bets.

By consolidating their consumer offering, Meituan-Dianping is able to then expand into additional verticals further afield, even if they're already dominated by established incumbents.

Meituan-Dianping's interlocking and complementary family of products gives it strength to move into otherwise implausible expansions into ridesharing and travel. By going after closer adjacencies first, they honed how they acquire, retain and monetize users, and can now leverage that built-in distribution to compete in more distant categories.

Yelp, Groupon, OpenTable, and UberEats in one super-app

Meituan-Dianping is the product of a merger in 2015 between Meituan.com (founded 2010) and Dianping.com (founded 2003).

After the merger, the combined company offered 4 core services:

A restaurant reviewing platform, similar to Yelp

A merchant deal platform, similar to Groupon

An in-store reservation, ordering and payment system, similar to OpenTable

A gig economy-style food delivery service, similar to UberEats and Postmates

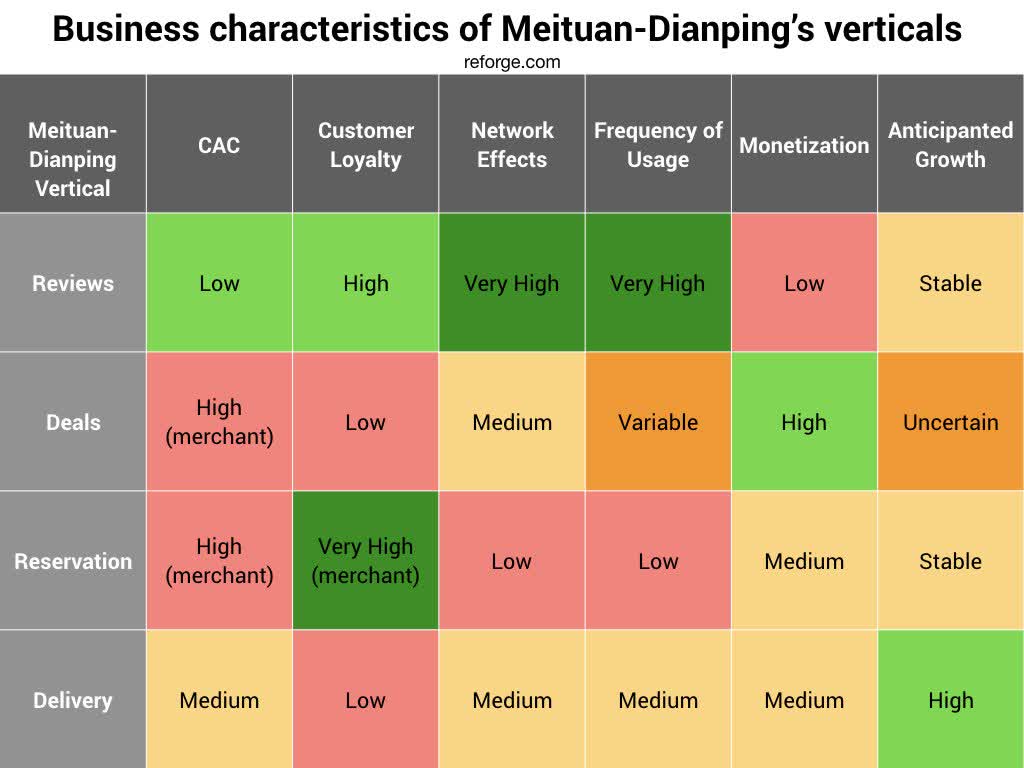

The table below gives you an idea of how Meituan-Dianping’s 4-vertical service offering breaks down in growth terms.

In the next section, we’ll go over the growth dynamics within each of these verticals, and how their aggregation contributed to Meituan-Dianping’s defensibility and core value prop to both consumers and restaurants.

Restaurant reviews — the traffic engine

Review platforms enjoy a data network effect that makes them hard to start, but also hard to displace once they’re established.

Dianping was founded one year before Yelp, giving the company an important first-mover advantage that helped make it the dominant restaurant review platform in China. High intent drives strong organic traffic, while user generated content keeps acquisition costs low. This enables (successful) review platforms to continue to acquire large audiences at low cost.

But, one traditional weakness of review platforms is that monetization tends to be misaligned with product. For example, Yelp has struggled with monetizing its userbase and faced widespread suspicion of manipulating reviews to please advertisers (which it denies).

Dianping, in merging with Meituan, sidestepped this problem by combining a traffic firehose with deals and delivery, opening up monetization pathways that aligned with consumer intent. Yelp has also tried for a similar approach, but: tried and failed to attack every other one of these verticals.

Yelp Deals ended up being an unsuccessful attempt to compete with Groupon.

Yelp Reservations (formerly Seatme) is having a hard time making significant inroads against OpenTable (their latest 10K showed less than 2M of revenue annually from Reservations).

Yelp sold Eat24 to Grubhub in August.

According to Yelp's latest 10K, 90% of their revenue comes from advertising, 9% comes from deals, 1% comes from reservations. The company hasn’t had an easy time diversifying out of their core advertising revenue stream because their competitors are too entrenched.

Restaurant deals — the monetization driver

Groupon in the US has faded in prominence in recent years, but restaurants in China still commonly use discounts and deals as a marketing and customer acquisition tool.

The same growth dynamics that powered the rapid growth of Groupon were also instrumental in its fall. Decreasing customer engagement led to diminished value to merchants, which made it harder to source compelling deals, which further decreased customer engagement.

This was in part because Groupon failed to own a compelling customer channel. The audience for daily deals have low purchase intent, and low conversion rates. Meanwhile, competition with other deal sites pushed customer acquisition costs up.

Through its merger, Meituan-Dianping gained a powerful customer channel that kept the deal ecosystem alive in China. Dianping brought huge amounts of organic traffic view its UGC reviews, and gave Meituan a cheap source of new customers with high intent (a person searching for which restaurant to eat at is a highly qualified lead for deals).

Meanwhile Meituan’s sales team could better monetize traffic than a review site alone by using it to bring in more and better quality deals. At the time of the merger, even though Meituan had only 1/10th the number of users as Dianping (20M vs 200M MAU), it was valued at almost twice as much ($7B vs $4B).

Restaurant reservations/ordering/payments -- a defensive moat for restaurants

Meituan-Dianping’s restaurant backend integration doesn’t have a direct analogy with any Western app. For restaurants that adopt it, users are able to make a restaurant reservation, order food and make a payment, all from within the app.

There are a few major challenges to integrating restaurant reservations, ordering and payments into one service:

Acquisition costs when targeting small businesses are high.

Time to successful activation is slow.

Small business go under frequently, which equals high churn on the platform.

These issues all eat into lifetime value, and make service aggregation tough. But, aggregation creates a defensive moat of loyal customers, because switching costs are also high.

Merging made it easier for Meituan-Dianping to sell integrated packages because Dianping’s merchant directory supplied a source of fresh leads while Meituan’s established sales team could convert those leads effectively.

But, the biggest value of this model was that it increased merchant loyalty. Merchants can sell on multiple deal sites, but in general they can only have one reservation system. Once a merchant adopts a reservation system, it’s much easier to convince them to use the same system for deals due to the stickiness of the integration.

By combining the two functions into one company, Meituan-Dianping’s salespeople are able to package a low margin, high retention product (the reservation system) with a high margin, low retention product (deas) and gain the benefits of both.

Restaurant delivery offers more room to grow

Because of the commodity nature of food delivery, customers tend to have high price sensitivity and low customer loyalty to any one delivery service. This is especially true in China where customers are far more price sensitive.

But, just 4% of overall dining spending in China is attributable to delivery, and the sector is seeing 200%+ YoY growth rates.

Restaurant delivery is the only vertical where Meituan-Dianping doesn’t (yet) have dominant market share. It owns 40% of the restaurant delivery market, trailing behind competitor Ele.me, which owns 53% of the market.

But even here, Meituan-Dianping has an advantage. Dianping (the review site) drives customer traffic straight into the arms of Meituan’s experienced sales team that’s already closing merchants for daily deals and reservations. This operational efficiency provides the company with a cost advantage over more siloed competitors, and it can pass that savings on to other areas of growth.

The future for Meituan-Dianping: ridesharing & travel

Meituan-Dianping has plans to move beyond food and restaurants and become a “lifestyle services company.” It’s rolling out a hotel review and booking service, competing with established competitor CTrip, and a ridesharing service, competing with Didi Chuxing, the #2 most valuable unicorn in the world (after Uber).

Although Meituan-Dianping faces an uphill battle in both categories, its review platform and logistics network will be useful assets as it takes on established competitors with natural defensibility.

Meituan-Dianping shows us an example of what could have been in the US. With each of the four verticals owned by a different US company (or multiple companies, as with food delivery), each has faced core weaknesses in their respective business models -- but each has also been so established that none of them have been able to outcompete each other.

In contrast, Meituan-Dianping has set up an interlocking and complementary family of products to make up for shortcomings inherent in any single business model, building itself a defensive moat and opening up strategic options for expansion.